Federal Student Loan Auto-Pay Users Get 1% Interest Reduction

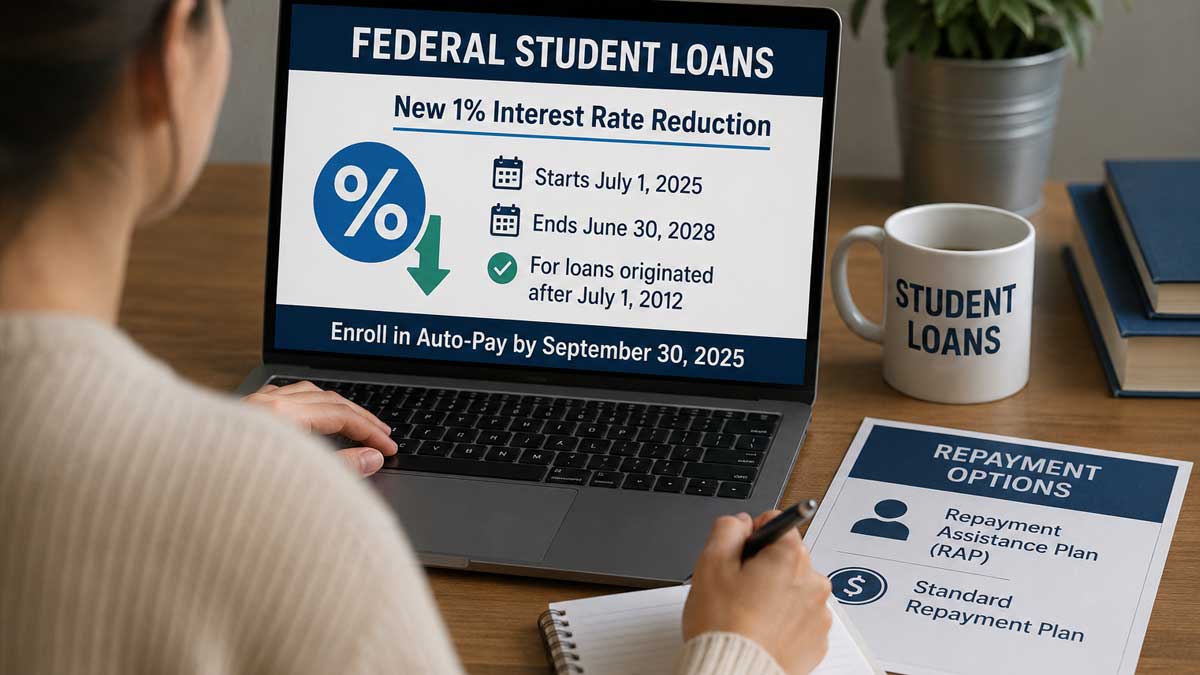

Federal student loan borrowers who enroll in automatic payments will receive a larger interest rate reduction beginning July 1, according to an announcement made Thursday by the U.S. Department of Education. The temporary benefit is designed to provide financial relief as significant updates to the federal student loan system are introduced.

Borrowers who already use auto-pay, which automatically withdraws monthly payments from a linked bank account, will automatically qualify for a total 1% interest rate reduction. Those not currently enrolled can receive the benefit by signing up for auto-pay before Sept. 30. The enhanced discount will remain available through June 30, 2028, and applies to federal student loans issued after July 1, 2012.

The new incentive expands upon the existing 0.25% interest rate reduction already available to borrowers using automatic payments, adding an extra 0.75 percentage points to the discount. Both student borrowers and parents with eligible federal loans can take advantage of the program.

Borrowers currently in default or those still enrolled in the discontinued SAVE repayment plan must first transition into a new repayment program before becoming eligible for auto-pay benefits. Individuals with defaulted loans may consolidate qualifying loans, enroll in a new repayment plan and then sign up for automatic payments.

The Education Department said the additional reduction will coincide with broader student loan reforms established under the federal government’s “One Big Beautiful Bill,” enacted last year. Among the most significant changes is the introduction of new repayment options for future federal student loan borrowers.

Starting July 1, borrowers taking out new federal loans will choose between a traditional fixed-payment repayment plan and the new income-based Repayment Assistance Plan, known as RAP. Existing borrowers, however, may continue using their current repayment programs if they prefer.

Officials noted that borrowers already enrolled in auto-pay do not need to take any action to receive the increased discount. The benefit will be applied automatically as long as they remain signed up for automatic payments. Borrowers who are not yet enrolled can still qualify if they activate auto-pay before the September deadline.

According to the Education Department, the percentage of federal student loan borrowers using auto-pay has fallen sharply since the COVID-19 pandemic. While more than 80% of borrowers previously used automatic payments, participation has declined to about 40%.

The Repayment Assistance Plan will replace previous income-driven repayment options for new borrowers. Under RAP, monthly payments will continue to be based on income, but borrowers must make payments for 30 years before any remaining balance becomes eligible for forgiveness. Previous income-driven plans generally offered forgiveness after 20 or 25 years. After July 1, RAP will become the only income-based repayment option available to new borrowers, alongside the standard repayment plan.

Additional provisions from last year’s legislation include new limits on federal student borrowing, tighter eligibility requirements for Pell Grants, restrictions on loan forbearance and the elimination of certain deferment options tied to unemployment or economic hardship. Separately, the Trump administration plans to implement new restrictions on the Public Service Loan Forgiveness program beginning July 1, limiting eligibility for employees of certain nonprofit organizations that do not align with government policy priorities.

Federal student debt remains a major national issue affecting more than 42 million borrowers. Efforts by the Biden administration to provide broad student debt relief faced legal challenges, and its signature forgiveness initiative was ultimately blocked by the Supreme Court. The Trump administration has taken a different approach, with Education Secretary Linda McMahon stating last year that “American taxpayers will no longer be forced to serve as collateral for irresponsible student loan policies.” The administration has also directed that the federal student loan portfolio be transferred to the Small Business Administration, although most loan operations remain under the Education Department. In addition, debt collection efforts on defaulted federal student loans resumed last year after a pandemic-era pause that had lasted several years.

Related Articles

Carrier Reveals Subsidiary Serviced Iranian Embassy After Acquisition

Carrier Global disclosed on Tuesday that a German heating company it acquired...

Lucid Shares Jump 20% After Saudi Prince Reveals $153 Million Stake

Lucid Motors shares surged Tuesday after Saudi billionaire Prince Alwaleed Bin Talal...

UEFA Weighs FIFA World Cup Boycott Over $4.2 Billion Investment Plan

UEFA is considering a boycott of future FIFA competitions, including the FIFA...

{kind=link}

Powerball Jackpot Climbs to $663 Million Ahead of Next Drawing

The Powerball jackpot has climbed to an estimated $663 million after no...

Leave a comment